Investing carries serious risks, including partial or total loss of capital. Please read the Key Investment Information Sheet and the Risk factors and login before investing.

A forecast P&L has been drawn, up to 2033 after closing clinical phase III, taking into account that CASC8 will not generate any turnover till the completion of clinical trial phase III.

Costs have been estimated and will roughly be covering R&D activities, the development of the CASC8 team and the protection of Intellectual Property Rights.

Followingcostswill be made:

1.2. Staff

The management team will be paid at a rate of €120,000 per year. The effort of these team members varies according to the need. The assumption is half time for the first phase. They stay a.i. until clinical trials and certification are completed. Then a new organisation will come into place.

Phase A: (2024 – 2025)

Two cell biologists will be hired as soon as the first R&D activities will start at an average salary cost of €6,000 per year. Also, an administration help is necessary preferably having some minor marketing skills. Cost 8k€/m, maybe halftime in the first 2 years. Then during phase A legal advice is needed (7k€), as well as a supply chain manager (7,5k€), all half time

Phase B: (2025 – 2029)

In phase B everybody out of Phase A will continue and become full time. For phase B the number of cell scientists will be ramped up from 2 to 11 FTE. As of 2027, a business developer will be hired. At the beginning of 2027, half-time and from 2028 onwards full-time at a cost of 10k€ per month

1.3. Project cost

Certification FAGG: 30k€

GMP production: 2023 - 2028

External cost of GMP facility for cell culture: - Testing engineering runs: 156k€ - Clinical trials: 52k€ per batch and per CASC treated patient

Phase A : Clinical trial I/IIa : 2023 - 2025

- 30 patients: 20 patients treated with CASCs + 10 control patients. - External cost of GMP facility for cell culture: see above - External cost of clinical centre: estimated at 12k€,000 per patient - External cost of CRO: €720,000 (estimated at €1500 per day) - External cost of Censtat of Hasselt University for the statistical analysis of the trial results: €20,000. - Consumables: catheter costs - 25 pts at 7,5k€/patient - Other: travel, equipment, fees - 225k€ - Tissue bank: 6,6k€ per patient

- 135 patients: 90 patients treated with CASCs + 45 control patients. - External cost of GMP facility for cell culture see above. - External cost of clinical centre: estimated at 12k€,000 per patient - External cost of CRO: €720,000 (estimated at €1500 per day) - External cost of Censtat of Hasselt University for the statistical analysis of the trial results: 60k€ - Consumables: catheter costs - 25 pts at 7,5k€

1.4. Miscellaneous costs

External advise: €60,000 per year

Patent costs: €8,000 per year

1.5. Revenues: forecast 2024 – 2033:

Forecasts were calculated only for the CASC8-track in 2 different ways:

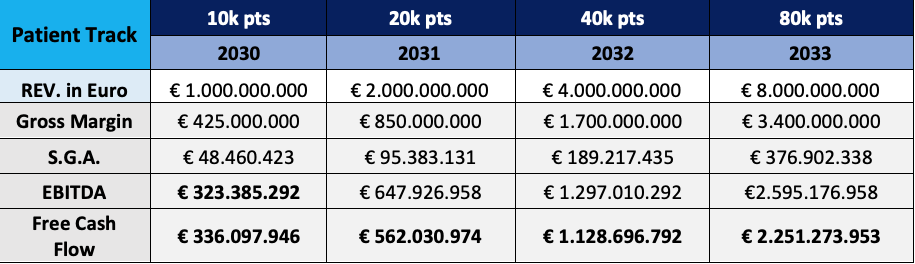

Patient track

- This track follows the general idea that the SOM is 0,5% of the total CHF population or 80.000 patients per year. This is even a small % of the yearly incidence. - The target is reached in a ramp-up of 4 years: 10k, 20k, 40 and finally 80k. - Cost calculations are explained above

patient track

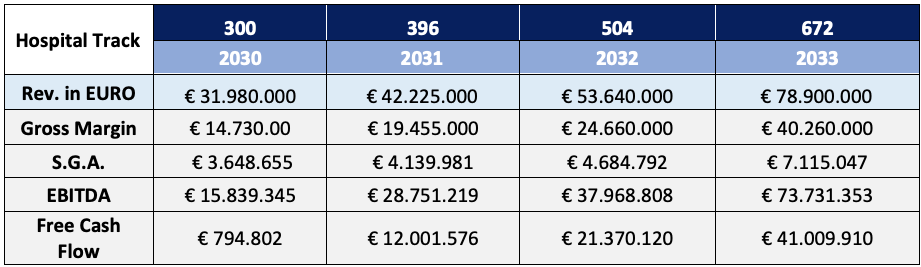

Hospital track

- Here the revenue streams are calculated starting from the 10 hospital centres that participated in the phase 2 of the clinical trials - Then from the sales activities a rhythm of 3 additional hospitals is started every quarter in the early adopter period. In the later early market phase this will double or triple. - Each hospital will, after the start-up phase treat 6 patients per quarter. - This will increase over time especially when logistics improve, and when closed incubators can be used.

Hospital track

2. Valuation

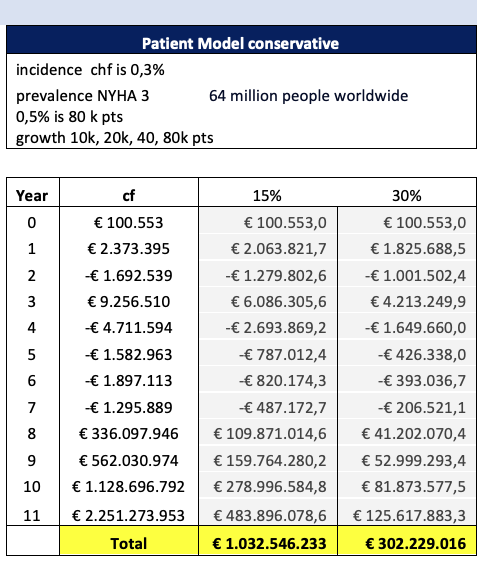

2.1. Discounted Cash Flow

It is rather premature to make a cashflow analysis and DCF.

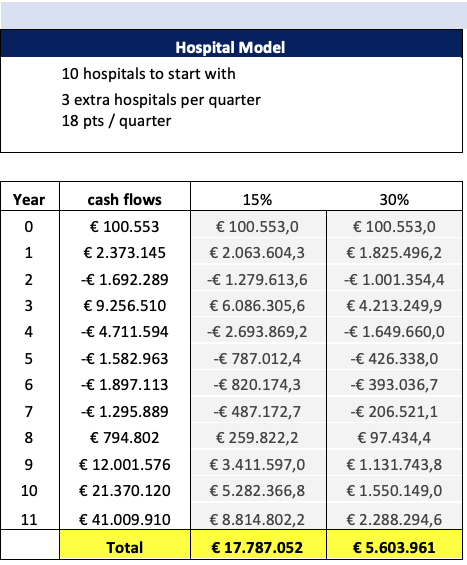

Just for indication: with a growth rate of 10%, average of industry, and a discount rate of 15%, the DCF brings us to an valuation from 18 mio€ to 1,03 bn€

Hospital model

patient model

2.2. Multiple short-term revenues: Revenues * 5

Calculated on the average of last 3 years, brings a valuation of 546,6 mio€

2.3. Multiple of EBITDA longer term:

The other rule of the thumb was EBITDA * 20.

More and more evaluators switched to a more reasonable *5.

What brings a valuation of 234 mio €

2.4. Benchmark

Many licensing deals and acquisitions have taken place in recent years in the field of cell therapy. Several examples of deals between biotech companies and large pharmaceutical companies have been described, showing that, in case of success, a good financial compensation can be obtained. This deal can take different forms, still to be decided, from an acquisition of CASC8, to milestone payments combined or/not with a license fee per patient treated.

An overview of past deals in regenerative medicine from 2012-2016 shows that biotech and device companies have been the most acquisitive, 5 times more than small to big pharma companiesxix.

In 2018 TiGenix has been acquired by Takeda Pharmaceutical for approximately €520 million.Takeda and TiGenix entered into an exclusive ex-US license, development, and commercialization agreement in July 2016 for Cx601, the leading investigational therapy in TiGenix’s pipeline. The candidate was a suspension of allogeneic-expanded adipose-derived stem cells. It is locally administered to treat complex perianal fistulas in patients with nonactive/mildly active luminal Crohn’s disease.

The latest report of ARM, the Alliance for Regenerative Medicine, the leading international advocacy organization dedicated to realizing the promise of regenerative medicines and advanced therapies, states that global financing in regenerative medicine will break records in 2020 (see Figure 3). In 2020, 204 clinical trials with cell therapy products were running, 49, 125 and 30 in respectively phase I, II and III. Forty-five of these trials fall in the domain of cardiovascular diseases.

For instance, Legend Biotech raised $487 million with a cell therapy for oncology (IPO). In follow-on offerings Iovance Biotherapeutics raised $604 million with an autologous cellular immunotherapy for tumour-directed Tumour Infiltrating Lymphocytes (TIL) and Atara biotherapeutics raised 2020 million with an allogeneic T-Cell Immunotherapy. The allogeneic cell therapy of Orca Bio raised $192 million in private financing.

3. Financial needs

The financial needs of CASC8 can easily be divided into 2 phases: